good receipt คือ: นี่คือโพสต์ที่เกี่ยวข้องกับหัวข้อนี้

The primary difference between Capital Receipts vs Revenue Receipts is that Capital receipts are the receipts of non-recurring nature which either creates the liability of the company or reduces the company’s assets whereas revenue receipts are the receipts of recurring nature and are reported in the statement of income of the company.

Table of Contents

Differences Between Capital Receipts and Revenue Receipts

Receipts are just the opposites of expenses. But without receipts, there may be no existence of the business. Not all receipts directly increase the profits or decrease the loss. But some affect the profit or loss directly.

In this article, we will be talking about capital receipts and revenue receipts. In simple terms, capital receipts don’t affect the profit or loss of the business; for example, we can say that the sale of long-term assets is one sort of capital receipts.

But revenue receipts affect the profit or loss of a company. As an example, we can say that the sale of products, the commission received, etc. are revenue receipts.

You are free to use this image on your website, templates etc, Please provide us with an attribution linkHow to Provide Attribution?Article Link to be Hyperlinked

For eg:

Source: Capital Receipts vs Revenue Receipts | Top 8 Differences (wallstreetmojo.com)

The nature and function of capital receipts and revenue receipts are completely different. In this article, we will do a comparative analysis of capital receipts vs. revenue receipts.

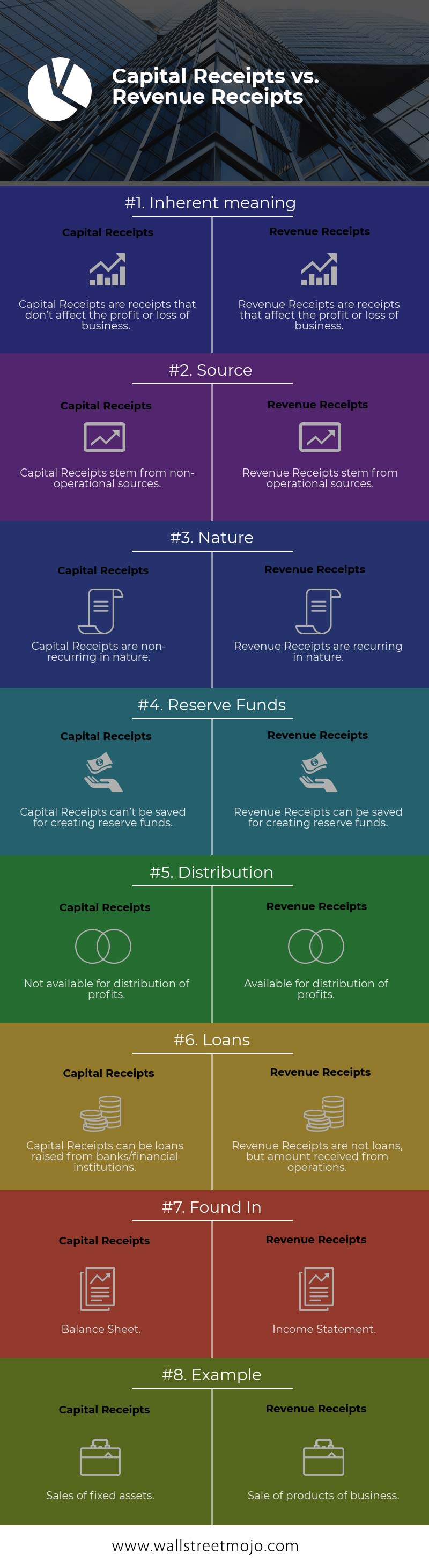

Capital Receipts vs. Revenue Receipts Infographics

There are many differences between capital receipts vs. revenue receipts. Let’s have a look.

You are free to use this image on your website, templates etc, Please provide us with an attribution linkHow to Provide Attribution?Article Link to be Hyperlinked

For eg:

Source: Capital Receipts vs Revenue Receipts | Top 8 Differences (wallstreetmojo.com)

What are Capital Receipts?

Capital receipts are those receipts which either create liability or reduce an asset. Capital Receipts, as mentioned above, are non-recurring in nature. And these sorts of receipts are also not received every now and then.

From the above definition, it’s clear that a receipt can be called capital receipt if it adheres to at least one of the following conditions –

- It must create a liability. For example, if a company takes a loan from a bank or a financial institution, then it would create a liability. That’s why it is a capital receipt in nature. But if a company received a commission for using its expertise in producing a special type of product for another company, it would not be called a capital receipt because it didn’t create any liability.

- It must reduce the assets of the company. For example, if a company sells out its shares to the public, it would help reduce the asset, which could create more money in the future. That means it should be treated as a capital receipt.

Types of Capital Receipts

Capital Receipts can be classified into three types.

-

Borrowing funds

When a company takes loans from banks or financial institutions, then it would be called borrowing funds. Borrowing funds from a financial institution is one of three forms of capital receipts.

-

Recovery of loans

To recover loans, often, the company needs to set aside one part of assets, which reduces the value of assets. This is the second type of capital receipts.

-

Other Capital Receipts

There’s a third type of receipts that we call “other capital receipts.” Under this, we include disinvestment and small savings. Disinvestment means selling off one part of the business. Disinvestment is called capital receipt because it reduced the asset of the company. Small savings are called capital receipts because they create a liability for the business.

Examples of Capital Receipts

Let’s now look at six examples of capital receipts. We will explain each of them and find out why they can be called capital receipts.

Capital Receipts Example: 1 – The money received from the shareholders

When a company needs more money, it can go for initial public offerings (IPOs). IPOIPOInitial Public Offering (IPO) is when the shares of the private companies are listed for the first time in the stock exchange for public trading and investment. This allows a private company to raise the capital for different purposes.read more helps a company to become public. When a firm gets public, then they sell their shares to the public. People who own the shares of the company are called shareholders of the company. Shareholders of the company hold shares of the company in lieu of offering money to the company. That means when a person purchases a share, he gives away the price of the share to the company. Through IPOs, the company earns a lot of money. And this money received from the shareholders can be called capital receipts because –

Capital Receipts Example: 2 – The money received from the debenture holders

When the company needs a lot of money, they go to people with bonds. The company issue bonds, and the debenture holders buy the bonds in lieu of money. The company promises the debenture holders that it will pay off the debt and a high interest within a certain period of time. These bonds are not backed by any collateral and especially dependent on the creditworthiness of the issuer. That’s why the interest rate is quite high. The money received from the debenture holders is capital receipt because –

- The money received from the debenture holders creates a liability for the company.

- The money received from the debenture holders is non-recurring in nature.

- The money received from the debenture holders is also non-routine, meaning it doesn’t happen every now and then.

Capital Receipts Example: 3 – Loans taken from banks or financial institutions

Often business needs to invest money to support any new project or partnership or expansion. But business always doesn’t have the money to invest. That’s why they go out to a bank or any financial institution to raise loans. These loans can be either secured loans or unsecured loans. The money received from these loans is then used for investing in the new project or for expanding their business. These loans taken from banks or financial institutions are capital receipts because –

- These loans create liability for the company.

- These loans are non-recurring in nature.

- These loans are not taken every now and then.

Capital Receipts Example: 4 – Sale of Investments

Let’s say that a company has invested some money into an investment fund. Now the company needs to influx some cash into the business. That’s why it decides to sell the investments to a buyer. Selling off the investments will help the company get some immediate money. And we will call it a capital receipt for the following reasons –

- Sale of investments reduces the assets of the company.

- Sale of investments is non-recurring in nature.

- Sale of investments is also non-routine.

Capital Receipts Example: 5 – Sale of Equipment

If a company sells out one of its equipment to get cash, it would be a capital receipt too. Here are the reasons why this is also a capital receipt –

- Sale of equipment decreases the value of assets of the company.

- Sale of equipment is non-recurring in nature.

- Sale of equipment is non-routine as well.

Capital Receipts Example: 6 – Insurance claim for damaged plant & machinery

Insurance can be claimed when the plant & machinery loses its value. And we can call it capital receipt as well because of the following reasons –

- Insurance claim means a reduction of assets of the company.

- Insurance claim doesn’t occur every day.

- Insurance claim is also not routine.

What are Revenue Receipts?

Revenue Receipts are those receipts that neither reduce the assets of the company, nor they create any liability. They are always recurring in nature, and they are earned during the normal course of business.

From the definition, it is clear that any type of receipt needs to satisfy one of the two conditions to be called as revenue receipt –

- First, it must not reduce the assets of the company.

- Second, it must not create any liability for the company.

Features of Revenue Receipts

Since revenue receipts seem to be the opposite of capital receipts, it makes perfect sense to look at different features of revenue receipts so that we can understand the meaning of revenue receipts and can compare to the features of capital receipts.

Let’s have a look –

- Means for survival: A business starts its operations because it expects to receive money as a result of their service to their customers. Either they can sell a bunch of products, or they can offer services. No matter what they do, without revenue receipts, they can’t survive for long because revenue receipts are collected from the direct operations of the business.

- Applicable for a short term: Revenue receipts are money received for a short period. The benefit of revenue receipts can only be enjoyed for one accounting year and not more.

- Recurring: Since revenue receipts offer benefits for a short period, the revenue receipts must be recurring. If revenue receipts don’t recur, the business wouldn’t be able to perpetuate for long.

- Affects the profit/loss: Receiving revenue directly affects the profit/loss of the business. When the revenue is received, either profit is increased, or loss is decreased.

- A small amount (volume): Compared to capital receipts, the number of revenue receipts is usually smaller. That doesn’t mean all revenue receipts are smaller. For example, if a company sells 1 million products in a given year, the revenue receipts could be huge and could also be more than its capital receipts during the year.

Examples of Revenue Receipts

In this section, we will look at six examples of revenue receipts. At the end of each example, we will investigate why this particular receipt can be called revenue receipt.

Revenue Receipts Example: 1 – Revenue earned by selling off waste/scrap material

When a firm doesn’t use the waste material or scram items, they decide to sell it off. By selling scrap items, the business earns a good amount of money. We will call it a revenue receipt. We will call it revenue receipt because of the following reasons –

- Selling off scraps doesn’t reduce the assets of the company.

- Selling off scraps doesn’t create any liability for the company.

Revenue Receipts Example: 2 – Discount received from vendors

When a firm purchases raw materials, they select vendors from whom they buy the ingredients. Often when the firm pays on time or early, vendors offer a discount. This discount received from vendors would be revenue receipt because –

- Discount received from vendors doesn’t reduce the assets of the company.

- Discount received from vendors doesn’t create any liability for the company.

Revenue Receipts Example: 3 – Services provided

When a firm provides services to its clients or customers, they earn revenues. We will call them revenue receipts since –

- Services provided to clients don’t reduce the assets of the company.

- Services provided to clients don’t create any liability.

- And it is recurring in nature.

Revenue Receipts Example: 4 – Interest received

If a firm has put its money in any bank or financial institution, it will receive interest as its reward. It is a revenue receipt because –

- It doesn’t create any liability of the company.

- It also doesn’t reduce the assets of the company.

Revenue Receipts Example: 5 – Rent received

If a firm offers their place to another company, they can collect rent, and it would be considered as revenue receipt for the following reasons –

- Rent would be received every month; that means it is recurring in nature.

- Rent received wouldn’t create any liability for the company.

- It would also not reduce the assets of the company.

Revenue Receipts Example: 6 – Dividend received

If the company has purchased shares for any other company, at the end of the year, if profit is made, the firm would receive the dividendDividendDividend is that portion of profit which is distributed to the shareholders of the company as the reward for their investment in the company and its distribution amount is decided by the board of the company and thereafter approved by the shareholders of the company.read more. This dividend received would be revenue receipts since

- It doesn’t reduce the assets of the company.

- And it also doesn’t create any liability for the company.

Also, have a look at Dividend Payout Calculations.

Capital Receipts vs. Revenue Receipts – Key differences

There are many differences between capital receipts vs. revenue receipts. Let’s look at the most prominent ones –

- Capital receipts are non-recurring in nature; on the other hand, revenue receipts are recurring in nature.

- Without capital receipts, a business can survive, but without revenue receipts, there is no chance that a business will perpetuate.

- Capital receipts can’t be used as a distribution of profits; revenue receipts can be distributed after deducting the expenses incurred to earn the revenue.

- Capital receipts can be found in the balance sheet. Revenue receipts can be found in the income statement.

- Capital receipts either reduce the assets of the company or create liability for the company. Revenue receipts are the opposite. They neither create the liability for the company, nor do they reduce the assets of the company.

- Capital receipts are non-routine. Revenue receipts are routine.

- Capital receipts are sources from non-operational sources. On the other hand, revenue receipts are sourced from operational sources.

Capital Receipts vs. Revenue Receipts (Comparison Table)

Conclusion

Capital receipts vs. revenue receipts are opposite, even if they both are receipts.

As an investor, you need to understand the distinction between the capital receipts and revenue receipts so that you can prudently judge when any transaction happens.

Understanding these two concepts also help investors make prudent choices about whether to invest in a company or not. If the company has fewer revenue receipts and more capital receipts, you need to think twice before investing. And if the company has more revenue receipts and fewer capital receipts (occurrence, not volume), you can take the risk because the company is now beyond the level of survival.

Recommended Articles

This article has been a guide to Capital Receipts vs. Revenue Receipts. Here we discuss the top difference between capital receipts and revenue receipts along with infographics and comparison table. You may also have a look at the following articles –

[NEW] Forwarder’s Cargo Receipt (FCR) | good receipt คือ – NATAVIGUIDES

When

freight forwarder acting as agents for the consignee, have received the goods

and all necessary documentation and payment of charges from the seller, freight

forwarder issues a Forwarder’s Cargo Receipt (FCR). The seller will use the FCR

to confirm to the buyer and/or the bank that he has delivered the goods for

shipment and that the carriage is being arranged by freight forwarder.

Freight

forwarder will arrange the ocean transport and the ocean carrier will issue a

Bill of Lading (B/L) or Sea Waybill (SWB). The Bill of Lading (B/L) or Sea

Waybill (SWB) is used to obtain release of the goods at destination.

It

is also possible to combine the use of the FCR with a House Bill of Lading (HBL)

or House Sea Waybill (HSWB) if the customer is using a NVOCC to supply ocean

carriage. If freight forwarder is the NVOCC and has issued a House Bill of

Lading (HBL) or House Sea Waybill (HSWB), there is no need to also issue a Forwarder’s

Cargo Receipt (FCR) unless there are specific reasons to do so.

In

many ways the Forwarder’s Cargo Receipt (FCR) document looks similar to the

Bill of Lading (B/L) and House Bill of Lading (HBL). But it is distinctly

different than a House Bill of Lading (B/L), Sea Waybill (SWB), House Bill of

Lading (HBL) or House Sea Waybill (HSWB) in that it does not evidence a

contract of carriage.

A

FCR cannot replace the Bill of Lading (B/L), Sea Waybill (SWB), House Bill of

Lading (HBL) or House Sea Waybill (HSWB). It is always used together with one

of these documents. A Forwarder’s Cargo Receipt (FCR) is issued by a freight

forwarder who is acting as agent on behalf of the consignee. We use Forwarder’s

Cargo Receipt (FCR) to facilitate payment.

When

the shipper has delivered his goods to the agent/freight forwarder (and any required

documentation), he will receive the Forwarder’s Cargo Receipt (FCR) as proof

that the goods have been delivered for shipment.

The Letter

of Credit (L/C) will stipulate which documentation must be in place before

payment for the goods will be effected. If the buyer and seller have agreed

that the Forwarder’s Cargo Receipt (FCR) is to act as proof that the goods have

been made available for shipment, the Letter of Credit (L/C) must clearly state

that payment can be effected upon presentation of a Forwarder’s Cargo Receipt (FCR).

The

advantage to the shipper of using the Forwarder’s Cargo Receipt (FCR) to effect

payment (instead of a Bill of Lading (B/L), Sea Waybill (SWB) or House Bill of

Lading (HBL) is that the Forwarder’s Cargo Receipt (FCR) can be issued before

the goods have been shipped by the ocean carrier. Therefore, the seller can

obtain payment for his goods faster than if he had had to wait for the Bill of

Lading (B/L) to be issued.

To

the consignee, there is an advantage when freight forwarder consolidates goods

from multiple shippers into one container. In such case, a separate Forwarder’s

Cargo Receipt (FCR) will be issued to each of the shippers but only one Carrier

Bill of Lading (CBL) or Sea Waybill (SWB) will be issued by the carrier. This

will save the consignee documentation and customs clearance fees at

destination.

When

a Forwarder’s Cargo Receipt (FCR) is issued by freight forwarder, the carrier

will issue a Bill of Lading (B/L) or a Sea Waybill (SWB). When a Carrier Bill

of Lading (CBL) or Sea Waybill (SWB) is issued, the shipper/seller under normal

circumstances has the right to amend the release instructions (i.e. consignee

name and destination).

By

accepting a Forwarder’s Cargo Receipt (FCR), the shipper assigns the benefit of

these forwarding instructions to the consignee (buyer). In other words, the

seller waives his right to revoke any delivery instructions after he has

delivered the goods to freight forwarder, and freight forwarder is not legally

obliged to comply with the shipper’s instructions after receipt of the cargo

and issuance of the Forwarder’s Cargo Receipt (FCR). Freight forwarder will

comply with the buyer’s instructions.

We

should note that although the Forwarder’s Cargo Receipt (FCR) is used as a

vehicle for payment, freight forwarder is not involved in the monetary

transaction and change of ownership between the seller and the buyer. Freight

forwarder issues the Forwarder’s Cargo Receipt (FCR) as a receipt for the

cargo.

Basically,

Forwarder’s Cargo Receipt (FCR) functions as:

The Forwarder’s

Cargo Receipt (FCR) is a receipt by the agent/freight forwarder that the goods

are in his custody. The Forwarder’s Cargo Receipt (FCR) does not confirm

shipment and can therefore be issued before the Carrier Bill of Lading (CBL)

has been issued.

The Forwarder’s

Cargo Receipt (FCR) does not evidence of a contract of carriage with the ocean

carrier, freight forwarder or NVOCC. The evidence of contract of carriage will

be the document issued by the ocean carrier (i.e. the Bill of Lading or Sea Waybill)

or the NVOCC (House Bill of Lading or House Sea Waybill).

The Forwarder’s

Cargo Receipt (FCR) is not a document of title. It cannot be negotiated, and it

cannot be endorsed to other parties. The consignee cannot be ‘to order’ and the

consignee’s name must be entered in full.

There

is no requirement that a Forwarder’s Cargo Receipt (FCR) is presented at

destination to obtain release of the goods. The release of the goods take place

based on the Bill of Lading (B/L) or Sea Waybill (SWB). In fact, the Forwarder’s

Cargo Receipt (FCR) is seldom used at destination. It is primarily a document

for origin use.

There

are 2 main areas of responsibility of an agent/freight forwarder issuing Forwarder’s

Cargo Receipts (FCRs):

The

consignee and the bank will rely on the description of the goods in the Forwarder’s

Cargo Receipt (quantity, condition, etc.) to effect payment to the seller. It

is essential that freight forwarder clearly notes any damages or shortcomings

on the Forwarder’s Cargo Receipt (FCR) or refuse to accept the cargo if the

physical goods received do not match the description.

Freight

forwarding acting as agents for the consignee, will arrange a Carrier Bill of Lading

(CBL) or Sea Waybill (SWB) that covers the carriage performed by the ocean

carrier. Freight forwarder should ensure that the description in the Carrier Bill

of Lading (CBL) or Sea Waybill (SWB) corresponds with the description in the Forwarder’s

Cargo Receipt (FCR). The consignee will expect to receive the goods as

described in the Bill of Lading (B/L) or Sea Waybill (SWB).

Freight

forwarder’s responsibility to care for the goods is closely related to what we

have just discussed. Freight Forwarder is responsible to take good care of the

goods while they are in his custody. If freight forwarder damage the goods,

freight forwarder become liable towards the consignee.

However

note that when goods are delivered to the carrier and covered by a transport

document (Bill of Lading or Sea Waybill), it becomes the carrier’s

responsibility to care for the goods. Freight Forwarder is only responsible for

the goods under the Forwarder’s Cargo Receipt (FCR) as long as the goods are in

his custody. This is distinctly different from a House Bill of Lading (HBL)/House

Sea Waybill (HSWB) where freight forwarder take on responsibility as carrier.

The Forwarder’s

Cargo Receipt (FCR) is not a document of title and an original is not needed to

effect release of goods at destination. As such, there is no reason why the Forwarder’s

Cargo Receipt (FCR) should be issued as an original document.

However,

often the shipper (and the bank) will insist to receive an original Forwarder’s

Cargo Receipt (FCR) and therefore the Forwarder’s Cargo Receipt (FCR) is often

issued in 3 originals and a reasonable number of copies. It is actually more

correct to issue 1 original Forwarder’s Cargo Receipt (FCR) and a reasonable

number of copies. But 3 originals is market practice in some areas of the world

today.

The

issuing agent should ask to have the original Forwarder’s Cargo Receipts (FCRs)

returned the shipper request an amendment to the Forwarder’s Cargo Receipt

(FCR). Amendments should be made in writing and are subject to acceptance by

the freight forwarder. The freight forwarder must ensure that no changes to the

description of the goods are made that can affect his position towards the

consignee.

SAP MB90 Print Goods Receipt

นอกจากการดูบทความนี้แล้ว คุณยังสามารถดูข้อมูลที่เป็นประโยชน์อื่นๆ อีกมากมายที่เราให้ไว้ที่นี่: ดูความรู้เพิ่มเติมที่นี่

SAP MM – Goods receipt without purchase order Mov type – 501

Goods receipt without purchase order Mov type 501

For SAP freelancing \u0026 Online SAP MM training contact on

https://www.linkedin.com/in/hrushikeshkaule05b15a60/

or

[email protected]

Hướng dẫn sử dụng SAP B1

SAP B1 Goods Receipt PO

Recorded with https://screencastomatic.com

Thao tác good receipt PO, Good returm PO

นอกจากการดูบทความนี้แล้ว คุณยังสามารถดูข้อมูลที่เป็นประโยชน์อื่นๆ อีกมากมายที่เราให้ไว้ที่นี่: ดูวิธีอื่นๆLEARN TO MAKE A WEBSITE

ขอบคุณมากสำหรับการดูหัวข้อโพสต์ good receipt คือ